Value signals in the orbitofrontal cortex incorporate reference-dependent news utility

Everyday we are faced with choices that yield hedonic responses. These responses are encoded in the brain as experienced utility signals, which can be found in the orbitofrontal cortex (OFC). These signals are used to learn the value of actions and stimuli, and affect memory encoding and retrieval. A key question in neuroeconomics and behavioral economics is what affects experienced utility. For example, is it influenced only by outcomes, or also by beliefs?

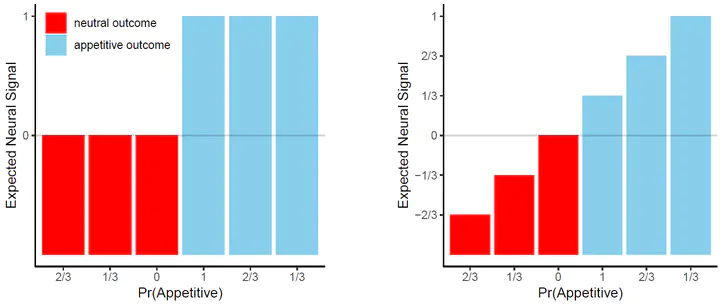

Behavioral economists have proposed expectations-based models of reference dependence that incorporate deviations from expectations (“surprise”) into experienced utility. Under these models, experienced utility can be represented as:

$U(x|p) = (1 − a) ∗ u(x) + a ∗ (u(x) − E[u(x)|p])$

where $a$ is a weight that captures the degree with which surprise modulates experienced utility, $u(x)$ is a utility function that captures the utility derived from consuming $x$, $p$ is the probability over potential values of $x$, and $E$ is an expectations operator. The first term represents the proportion of experienced utility that is the direct pleasure derived from consuming x (i.e. the “consumption” component). The second term represents the proportion of experienced utility that is derived from the deviation of experienced pleasure from ex ante expectations (i.e. the “surprise” component).

Although this class of models have become quite influential in behavioral economics, and are capable of explaining some puzzling phenomena, the fundamental assumption that experienced utility depends on both consumption and surprise has not been tested. Here, I propose to combine fMRI with a carefully designed task to test this approach.